Tick tock – Why private business owners with less than 4 year exit horizons should reassess timing now

29.5.2026There was plenty of market chatter prior to the budget speech this year. Investors and asset owners were nervous. We had a client pushing for a deal to be signed before Budget Day. We managed to get this done, just in time. Several others in the business ecosystem spent the Mother’s Day weekend scrambling to sign deals, employee incentive schemes and lock-in other equity transactions. And then on Tuesday, the Capital Gains Tax (CGT) changes were announced. It may not have been a big surprise to the market, but post-announcement, the disapproval, backlash and rage was evident on social media. These were significant changes.

Incremental minor changes to the tax regime are generally accepted easily by one and all. Large-scale changes often create nervousness in the market and reduce investment confidence. The economic implications of large-scale tax changes cannot be calculated, only estimated at best. The more significant the changes, the lower the confidence in these estimates and in desired economic and social outcomes of the changes.

Amongst the several other changes proposed, the government will abolish the 50% CGT discount from 1 July 2027, replacing it with cost base indexation and a 30% minimum tax on net capital gains for assets sold after that date. Transitional relief preserves the 50% discount on gains accrued up to 1 July 2027 for assets already held, meaning owners will need to establish the market value of their assets at that date to split gains between the old and new regimes.

In a global economy, where Australia is competing for financial and human capital, the recent changes may impact the country’s ability to secure these critical input resources. The macro-economic risk is that other first world nations will lure Australian talent e.g. our future entrepreneurs, business owners and top corporate executives. Whether this brain drain will occur remains to be seen. We are already seeing investors discussing New Zealand, Singapore, UAE and other alternatives to Australia. We are being asked what the near to medium term impact of the budget will be on M&A activity.

In the listed company landscape in Australia, retail investors account for 20% to 30% of the cumulative market capitalisation. Super funds and institutions, which account for the remainder, are not likely to be affected by the budget changes and as their return expectations will not vary because of the CGT changes. In the ASX-listed landscape, transaction activity may be impacted differently for small and micro-cap companies vis-à-vis mid and large-cap ones. M&A activity involving companies with significant shareholdings of institutional investors, superfunds, foreign investors may be rather insulated from the proposed CGT changes. This would include most ASX mid-caps and large-caps and mid-caps. The marginal price on large-cap stocks, which is set by institutional capital pools, is not expected to see a change post-budget. As such, boards of listed companies/ other large institutionally held companies, may not see 1 Jul 2027 as a critical date. For listed companies that have a significant retail investor base, the impact is less straightforward. Demand and supply dynamics from retail investors may be quite complex. While there is an argument that the increased CGT will increase the expected return post 1 Jul 2027 and create a downward pressure on share prices, this needs to be considered in the context of risk/ return profiles of alternative investment options including real estate, all of which will be impacted by the CGT changes to varying degrees.

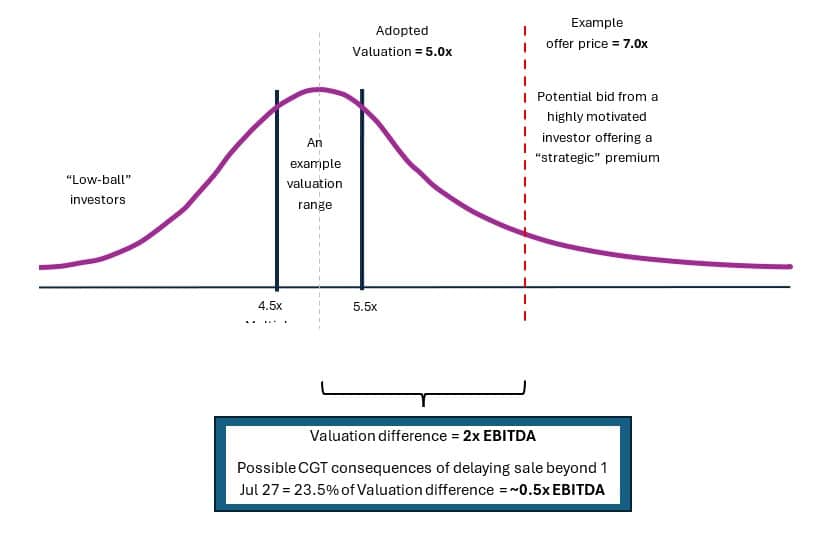

The ‘Transitional’ regime may impact the thinking of privately held and family businesses around a liquidity event. The valuation of the business as of 1 Jul 2027 will be an important number for such businesses. For listed companies and property, valuation will be straightforward because of automatic price discovery through market trades. For operating businesses, valuation is more obscure and open to professional judgement of the valuation expert. Business owners may be concerned about a valuer ascribing a value to the business which is well below what they think the strategic value is. In this context, it is worth mentioning that sale processes may yield a spectrum of bids/offer prices which are a function of the ‘value’ of the target business to the bidder (e.g. a financial bidder may ascribe a lower value to the business than a strategic party that may enjoy significant synergies, may ascribe to it). If bids/ offers followed a normal distribution, strategic bidders would offer a significant premium to the mean value. However, a valuation exercise will normally result in a value or valuation range that is closer to a ‘mean’ value of such bids, as a valuation exercise doesn’t ascribe any strategic premium for synergies. To quantify the CGT impact of this disparity, if a strategic bid results in a value that is 1 to 2 turns of EBITDA higher than an independent valuer may ascribe (e.g. a strategic buyer may offer 7x EBITDA for a business, while a valuer may assess value at 5x EBITDA), then there is a potential tax leakage of approximately 0.25x to 0.5x EBITDA if the business is sold after 1 Jul 2027.

Also, valuations can be expensive and may be open to challenge by the ATO. If business owners have a long-term investment horizon, the CGT changes may not and arguably should not drive them to bring forward a sale or liquidity event. However, for business owners that have a 1-to-4-year exit horizon, the CGT changes may well result in them bringing forward their sale processes. In my view, there will be a spike in private company M&A activity in the lead up to 1 Jul 2027. But this surge in activity may be followed by a cliff as motivated vendors who miss the tax transition date withdraw from the market. Another element to note is that if vendors leave things too late and negotiations with counterparties continue beyond May 2027, vendors may lose their bargaining power in negotiations, as they will likely have to make commercial concessions to ensure deal signing prior to 1 Jul.

If you’re a business owner, shareholder or board member of a privately held business, it is worth exploring whether there is merit in bringing forward a sale process considering the recently announced CGT changes, while ensuring that your planning allows enough time for a process. A sale process typically takes 7 to 12 months. We would be pleased to have a confidential conversation about your business, growth strategy, exit aspirations and discuss a typical sale process.

Reach out to the InterFinancial team for a confidential discussion about your options and the opportunities ahead.